Back from India! Bullish $CRESY and Short $TRUP

Argentinian farmland and a pet insurance company.

Hello everyone!,

I am back from India and what an experience it was. It could be described as the land of extremes. From marvelous landscapes and architecture in Udaipur and Dehli, great food and vast wealth to extreme poverty. Heartbreaking, stunning and amazing. India is a roller coaster of emotion. I had both great and terrifying moments there, but overall it was a good experience. Being amazed that anything gets done, given the often lacking infrastructure - I started to research Indian stocks.

Looking at several of them, I was impressed by the quality of companies, but the prices reflected that. Compared to other emerging markets, and even their own valuation, India is very expensive.

I would not short India, but it is out of my comfort zone. I usually like to invest into companies or countries that have a potentially bright future and are cheap. India certainly has the former, but sadly not the latter. I will have a look, once the PE is around 12.

Market Thoughts (can’t escape those)

Everyone asks about Macro. Instead of looking individual companies, everything seems to be a derivative of central bank actions. Portfolio's with the conventional wisdom of 60% stocks and 40% bonds have their worst YTD return in the past 100 years and the price action in a 20 year treasury bond ETF (TLT) looks more like Bitcoin than a safe haven. Innovative companies that were money incinerating are often down 70%+ and even the mighty S&P500 has fallen more than 20%. The only positive sector is energy.

I still believe that we are going to see strong inflation of around 4-5% for the next decade. We might have peaked in intensity, but not overall. We have seen deglobalization starting before the pandemic, and its pace has only increased. This is strongly inflationary, and will require huge amounts of energy and materials. Countries that do well during a commodity bull market will have great returns. Brazil for example would be one of them.

As everyone is a macro investor now, it is important to weigh risk/reward. Druckenmiller shorted the pound in 1992, making one billion in a single day. This was an extraordinary opportunity. Not only because of the size, but also because of how skewed the risk was compared to the reward. If after 6 months, the pound would not have devalued - the fund would have lost 0.5% - if he was right, he made 20%. Betting on a direction of currencies, markets or interest rates can be incredibly rewarding and exciting - but more often than not, the risk/reward is not very attractive. This is in contrast to a lot of individual stocks today. As the market declines, I find more and more companies being attractively priced.

One of them is Cresud Sociedad Anónima, Comercial, Inmobiliaria, Financiera y Agropecuaria or $CRESY for short. It offers the cheapest farmland in the world by far in Argentinia. There are the obvious Argentinian risks. Here is a great writeup. Thanks @SandbergHaedo for the research.

https://seekingalpha.com/article/4528459-cresud-agri-stock-everything-you-need-to-know-about-it

Not just in emerging markets like Argentina or Brazil, but also in countries like Japan - where companies that are export power-houses like Itochu are quite cheap given the decline of the yen. I am not yet a buyer on those export companies yet, but they do look interesting. I am starting to put some research into Columbian equities. Here is a great substack article describing the bull and bear cases for Columbia.

At the same time, we have a lot of unprofitable growth stocks, still trading at insane multiples offering us short opportunities. One of them is Trupanion.

Trupanion an insurance company at SaaS valuations

If you look at the graphs that the Trupanion management publishes, its hard not to become optimistic. An insane increase in revenue for this pet insurance company. Yet not all is rosy behind the scenes.

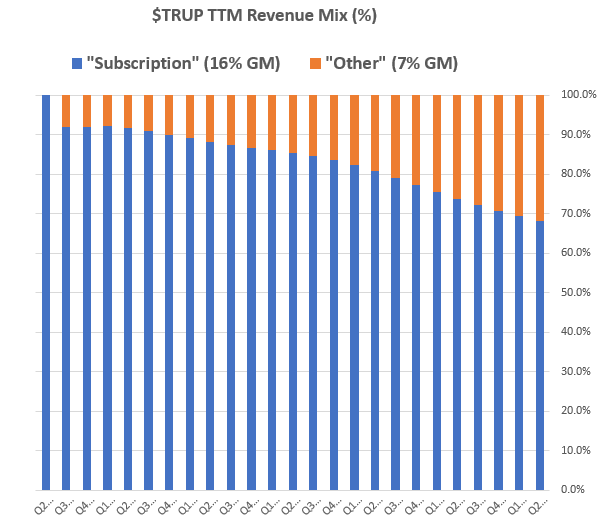

Trupanion is a pet insurance company that pretends it isn't. While the revenue increase is impressive, the earnings aren't. Since becoming a public company in 2014, the company has only reported six quarters of positive operating income. Even more concerning is that the company's gross margins are getting worse and they operated in pet insurance, which was neglected by the big players until recently. Furthermore, the loses in a quarters are increasing.

Trupanion pretends to not be an insurance company

That starts with their earnings releases. Instead of reporting the common premiums earned/loses incurred that is usual with insurance companies, they report it as subscription business. That just means that one needs to go to NAIC, to get a better picture of the financials.

According to NAIC, The American Pet Insurance Company (The underwriter and subsidiary of Trupanion) in 2021 had 581.5m of earned Premiums, and 379.9m in losses occurred. That means that the loss ratio of their underwriting is at 65% (Incurred loses/Earned Premiums). The average loss ratio in this space is around 50%. They also had 167.4m in underwriting expenses. So the Expenses Ratio (Underwriting Expenses / Earned Premiums) is at 28.78%. That would bring the combined ratio to 93.78%. Which is decent for an insurers. Everything over 100% means that the company loses money on their underwriting abilities. However the financials that Trupanion reports make it incredible difficult to analyse.

In their 2021 10k, they report 494m in "subscription" business with a cost of 407.6m, which would bring the loss ratio to 82%. As they have other parts of the business, we only take 60% of Technology and SG&A expenses. With the New pet acquisition that would bring the total expenses to 107.8m. They lease out part of their owned buildings and record that within SG&A instead of revenue, which was $1.1m in 2021. Using all that, the expense ratio as a result to 21.9%. So the combined ratio here is 103% - bringing their underwriting expenses into negative territory. Insurance is a business of variable cost and does not offer the inherent scale advantages of Software. Looking at Trupanions numbers should confirm that there is no torque to more revenues.

As the earned premiums of their insurance company are higher than those reported in the subscriptions section of the earnings statement, it means that the company seems to underwrite for other companies as well. Indeed the low gross margin in other is probably some of that underwriting tucked into there. Thanks @Keubiko for the graph.

The big expenses are obviously the Pet acquisition costs. These are an integral part of the business. Trupanion shows us the average monthly retention of 98.75%. Impressive at first sight given that a lot of insurers in the US have a retention rate of around 84%. However those are annualized. Using the 1.25% monthly churn rate and using it in the math expression 1-((1-Churn.Monthly)^12), we get a retention rate of 85.9%. This looks good at first sight, but we need to remember that they are pets. Trupanion calculates that the average pet is with them for 79.4 months or around 6.5 years. As Trupanion only offers pet insurance, they can't lock their customers in or up-sell them into other insurance products. Thus they need to spend money to acquire each new pet. This is more important than ever as competition increases. JAB recently acquired the pet insurance business from Fairfax, consolidating part of the industry.

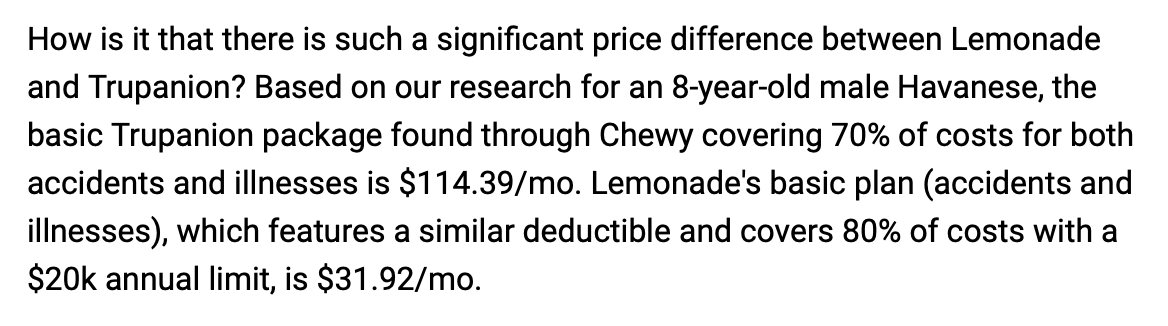

According to ValuePenguin, Trupanion is now among the most expensive options for pet insurance. Chewy, the pet supply company recently announced a partnership with Lemonade offering pet insurance. Chewy already has a partnership with Trupanion. When the Chewy/Trupanion partnership was announced, Trupanion surged nearly 40% in December 2021. The Lemonade offering is much cheaper than the Trupanion one. Both cover accidents and illnesses, but Trupanion covers 70% of the costs at $114/month and Lemonade covers 80% with a $20k annual limit at $31/month. Thanks @PaperBagInvest and @coverager for the info.

Given the huge discrepancy between the two offerings, Trupanion looks like it has priced itself out of the market. They will need to change their underwriting approach and spend more on pet acquisition costs. Given that they aren't profitable now, what will happen when they need to cut their earned premiums?

Insider selling and increased compensation

Usually putting a lot of weight onto insider selling is futile. There are many reasons to sell. The exception are serial sellers in my eyes. Carvana comes to mind, where the executives were selling millions of shares each week. Trupanion falls into the same category. Since 2014, the CEO hasn't bought a single share in the open market, and sold more than $42m. Each week like clockwork he sells 4000 shares, increasing the sell orders significantly this year. Thanks @PD13158196! But the rest of the executives are selling as well. Since going public, the sales amount to $123m wheras the buys total only $2.5m. I have nothing against insider selling, if the company is profitable - but if they had close to a decade and not a single year where they reported a profit, I get cautious.

Trupanion only had six positive quarters in nearly a decade of operations. In those six quarters they generated $4.91m in operating profit. That means that the CEO sold 8x more in shares than the company generated in operating profits in its history. Conveniently the CEO just sold days before the Chewy and Lemonade partnership became public. How fortunate. Furthermore the executive compensation increased by crazy amounts from 2021 to 2020. The pay of the CEO increased by 420%, the president's pay by 440%, the COO's by 430% and the two vice-presidents by at least 250%.

Given that the losses have gotten worse, not better - this should be worrying for investors.

No return to shareholders

Insurance companies are usually know to pay a reliable dividend. Trupanion has never paid a single cent in dividends and according to their latest filing doesn't plan to do so. Furthermore, the company has diluted shareholders. Since 2014 their share amount doubled and they dilute by at least 3.5% yearly (11% in FY 2021).

Given that the S&P 500 pays out around 1.6% yearly in dividends and has returned 10.05% since 1926. How will you get a better return given no dividend, no profitability and dilution?

Huge multiples

No return to shareholders, insiders selling and hard to understand financials. Are you sure you are not talking about CRESY until they started a buyback program recently?

Well yes. I have no problem buying into questionable companies, as long as I think that the price reflects that. It needs to be cheap if the quality isn't there. Sadly for Trupanion, the multiple is anything but cheap. Trupanion still trades at 7.2x P/B. That is very expensive for an insurer. The average insurance company in the US trades at 1.5x P/B. Even the best ones like Admiral trade at 5x P/B. However Admiral has a combined ratio of 85%, pays nearly 5% dividends, and have been growing earnings (so not just revenue) 12% yearly for more than a decade. Most of the best insurance companies trade at 2-3x P/B. Admiral justifies it's premium with shareholder returns. Trupanion doesn't. Unprofitable insurance companies trade closer to 0.8x P/B.

So assuming that Trupanion becomes a great insurance company and trades at 3x P/B, it would bring the share price to $20.4, assuming no further dilutions. That is close to a 60% downside. And that is the bull case. Even if you factor in earnings growths in your model, there is at least 40% downside left.

If you assume that they start to get valued as an unprofitable insurance company at 0.8x P/B, we would be at a share price of $5.45 or close to 90% downside.

Conclusion

Trupanion is tremendously overvalued given the obscure financials, increased competition, shareholder dilution and P/B ratio. Given that competition is increasing and the CEO is increasing his equity sales, it is difficult to be anything other than bearish on this name.