Learning from Soros, Am i a permabear? Doordash Share Buyback, Strip clubs as economic indicator, Reading academic papers and more

Tiktok Investors levered to the hilt, Watch prices declining, investing without prejudice and Horizon Kinetics market commentary

Good morning Coffee drinkers and tea lovers alike!

Today we will cover a wide array of topics where we go from interesting to substandard in the span of a few paragraphs.

Learning from George Soros

Learnings of two papers (Bitcoin as diversification, chasing returns)

Investing without prejudice and Kaspi's buyback.

Am I a perma bear?

Horizon Kinetics market commentary

Doordash share buyback program

Levered Tiktok investors

Stripers as economic indicator and Watch prices declining

Learning from George Soros

For me George Soros and Stanley Druckenmiller are among the best speculators of all time and I take every chance I can to learn from them. This lecture from 2009 provides great insights and should be watched. Here is a quick summary.

Efficient market hypothesis is wrong. Market prices always distort the underlying fundamentals (we could see that AMC and GME were saved from bankruptcy through issuing stock during the meme-craze).

Those distortions can vary in significance and often create positive reinforcements.

That reinforcement leads to bubbles, which reaches a climax and reversal points, which then reinforces itself in the other direction (we are seeing this now, with the quick drop of those meme stocks and crypto).

Bubbles always have an underlying trend and a misconception. Once that misconception gets so far from reality, market participants need to admit that they were wrong. They are dancing until the music stops and then everyone wants to get out quickly. (we might see that soon with Tesla stock).

The length of that bubble is unpredictable, but the sequence of reinforcement -> climax -> reinforcement is always the same unless the government or negative feedback intervenes.

The efficient market hypothesis is also wrong, because securities get priced based on the future. As the future is unknowable, those prices are not correct and often overshoot both the upside and the downside.

Historical events, which outcomes are uncertain also disrupt the statistical generalisation (we saw that in 2020 with the pandemic and now with the Russian invasion of Ukraine).

In extreme cases like the Great Financial Crisis all risk management tools and synthetic products which rely on the statistical generalisation will break down and hurt investors - but they also create tremendous opportunity.

Due to the very high volatility during the GFC, he had to reduce his position at the wrong time. Smaller positions and sticking with them would have been the better outcome. Increased volatility requires a reduction in risk exposure as forced liquidations can distort prices to both the up- and the downside.

Markets are always bubble prone due to human nature.

Markets are potentially unstable due to systemic risk that gets ignored by nearly all investors.

What needs to be done in the long term is often wrong in the short term (from both investors and regulators).

While the video quality of this lecture puts a clear date on it, the contents are priceless. We are currently seeing the reversal of bubbles in the high-growth companies and even the index and the focus shift towards energy. I think it is likely that energy will bubble in this decade just like technology did. Looking at what was hot over the last decades, not a single one carried over to the next. Reading through newspaper headlines at the time the shift seemed sudden and unexpected, while the news of today point how obvious that shift was in hindsight. The only thing that we can do, is look at the numbers as unbiased as possible and take in the mantra of Stanley Druckenmiller:

Strong convictions, loosely held

Learnings from two academic papers

I have started to read academic papers in the last few weeks mainly those that are recommended by WifeyAlpha on twitter. While a lot of them are only relevant for quant investing, several of them have great insights.

Safe haven or risky hazard? Bitcoin during the Covid-19 bear market

I never had interest in Bitcoin as a store of value or currency - but it would be interesting as an uncorrelated asset as Ray Dalio so often preaches. This paper looks at the crypto bear market during the pandemic and if Bitcoin was an uncorrelated asset or safe haven. As expected the S&P500 and Bitcoin move in lockstep and thus increasing the downside risk for investors with an allocation to Bitcoin.

This paper does not include the remarkable correlation of the Nasdaq with Bitcoin. In the following chart we see a 3x levered Nasdaq (TQQQ) in blue compared to the Bitcoin market cap and they look eerily correlated.

This sadly means that Bitcoin becomes completely uninteresting to me, as it now isn't even an uncorrelated asset.

Asset Allocation and Bad Habits

This is a great paper about asset allocation and bad habits in investing. It proves that both retail and institutional investors are momentum investors without realising it. They chase returns ignoring mean-reversion and buy into the recent longer-term winner asset classes or managers. This reduces their performance. Here is a quote i found very insightful.

Institutional investors may be especially pro-cyclical at three- to five-year horizons, reflecting their typical performance evaluation periods.

It also shows that as they chase the returns, the returns are good in the first year, but decline then. We saw the same thing with the ARK Investment funds.

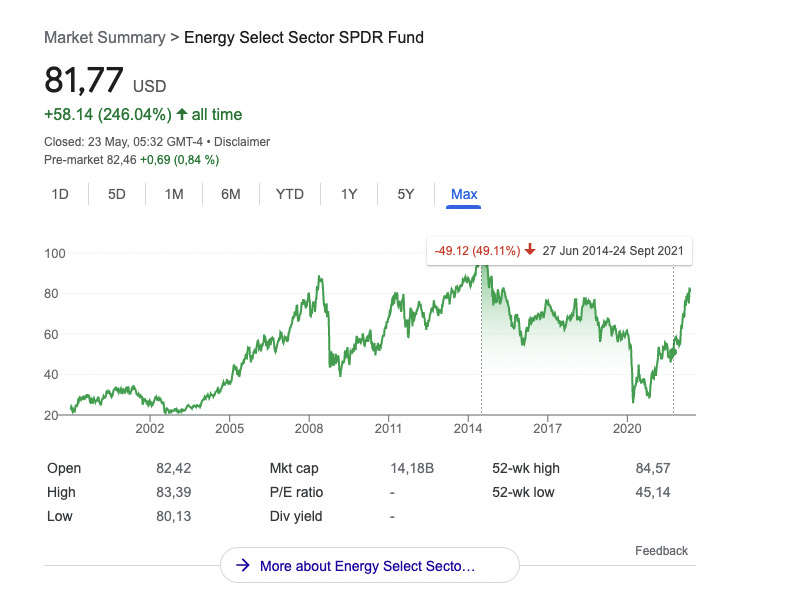

Harvard's endowment fund said that they will divest all holdings in fossil fuels in September 2021. This move is not only due to global warming, but also because of the horrible returns that Energy had over the last few years.

From the top of 2014, to September 2021 the XLE - an ETF selected Energy stocks returns a whopping -49%. Incidentally, the article might timed the bottom of the 7 year move. We see clearly that investors judged by 5 year returns, would divest from such an asset class - regardless of climate change. Looking at the return since then, we might see more inflows again into energy. Given that they are judged by 3-5 year time horizons, we might need to wait a few years until that time comes.

Investing without prejudice and Kaspi's buyback

Ilya Kan, who wrote an excellent piece on Kaspi, is quickly becoming one of my favourite Substack authors.

He wrote, that he recently met a hedge fund manager who invests into similar securities as he does, and who was appalled by investing into Kazakhstan. Mental barriers often hinder us from investing into the most obvious places. Kazakhstan is a foreign land and lots only know the country from the movie Borat (which is hilarious to be honest). But reducing a country to its stereotypes, prejudices and past often overlooks the developments and the beauty that lies within. Kazakhstan with 18m people is not small and it has big natural resources like oil and uranium. With Kaspi it now also has a strong technology leader and I think that the future for them is bright.

Kaspi has been recently buying back shares at low prices. Even tho the share buyback is far from the $100m announced, it looks promising given that they are profitable and their Ukraine expansion plans has been halted. I think Kaspi will be a great investment for the next few years.

Am I a perma bear?

I have been very vocal both on Twitter and on Substack with mostly bearish takes. Liberty shared a post, that pessimism nearly always sounds smarter:

Interesting piece by the excellent Jason Crawford:

I’ve realized a new reason why pessimism sounds smart: optimism often requires believing in unknown**, unspecified future breakthroughs—which seems fanciful and naive**. If you very soberly, wisely, prudently stick to the known and the proven, you will necessarily be pessimistic.

This is so true.

You can point to problems — there! Look at that horrible situation! — but you mostly can’t point to solutions, *because if they were already here, the problems would’ve been solved already*…

In just the same way, it can seem that we’re running out of ideas—that all our technologies and industries are plateauing. Technologies do run a natural S-curve, just like oil fields. But when some breakthrough insight creates an entirely new field, it opens an entire new orchard of low-hanging fruit to pick. Focusing only on established sectors and proven fields thus naturally leads to pessimism. To be an optimist, you have to believe that at least some current wild-eyed speculation will come true. [...]

But if progress is a primarily matter of agency, then whether it continues is up to us.

Its true, I am pessimistic regarding the valuation of growth-stocks and in general the US market. I am however also optimistic regarding the returns in energy companies, small companies in Japan and emerging markets like Argentina, Brazil and Kazakhstan.

Overall I am optimistic that the process of the last century will be accelerated with computers and new technologies. There are some companies that I would love to own (like Elastic Search, $ESTC), but that are just too expensive for my liking.

So no, I am not a perma bear - I just try to manage my own expectations. To sum it up in a sentence: "Lowering my expectations in order to minimise the level of disappointment."

Horizon Kinetics market commentary

I always look forward to read Horizon Kinetics' quarterly letter and this one is no exception. In it, they lay out that the current inflation environment is different compared to the one in the 70s, due to the different in debt to GDP level (around 35% then vs 125% now) and that the US can't service its debt - if it hikes rates too much. Definitely worth a read.

Doordash announces share buybacks

Doordash recently announced a $400m share buyback program. The food-delivery company only had one profitable quarter back in 2020 and is still valued at $23b. The stock is down nearly 75% since its peak in November 2021. While this buyback program goal is to stop the stock decline and looks good at first sight, it is the exact opposite. Doordash investment thesis is strong strong growth. The company has a $3.6b cash/short term investment cushion to strive towards that goal. Since they are not profitable, they deplete their cushion by buying back shares and admitting that their growth story is no more. This is different compared to Kaspi, which is profitable and uses some of their excess profits to return value to the shareholders.

When a stock is down 73%, it looks like the easy money on the short side has been made. Then I refer to David Einhorn's quote:

“What do you call a stock that’s down 90%? A stock that was down 80% and then got cut in half.” - David Einhorn

Bloomberg wrote in March, that the rapid wage growth in the US isn't going anywhere soon. While the wage growth might be below inflation it is devastating for companies like Uber and Doordash who rely on cheap labor for their business models. By initiating this share buyback Doordash has admitted that the thesis is broken, and might now be an easier short than at its peak at $245. As the S&P500 has now closed declined 7 weeks in a row, a bear rally might give a nice opportunity.

Tiktok Investors levered to the hilt

A Tiktok video is making circles around my Twitter sphere. A couple is taking private loans to flip property. According to them, those loans are 8-12%. Those are extremely expensive loans especially in the real estate realm.

House prices in the last few years have been exploding. The average sales price rose 34% in the last two years. With that movement those loans seem to make sense, but they don't.

Looking at the Case-Shiller U.S National Home Price index from 1928 to 2022 the price on average increased around 4%. This move then looks incredibly risky as the odds are stacked heavily against you making any returns.

This reminds me of the scene from big short. "Why are they confessing" - "They are not, they're bragging". It is best to be cautious of leverage in the best opportunities, and one should stay far away if the odds of reward are so stacked against you.

Strip clubs as economic indicator and Watch prices declining

In the same Twitter sphere, we have a strippers posting that the strip club is a leading economic indicator. Other that we are playing limbo with the quality of this article, I find it very interesting given that watch prices are also declining. While inflation might not have reached the affluent people who can afford these watches, they seem to reflect on how they spend their money. Watches and strip clubs seem to get removed from that equation. RCI Hospitality Holdings ($RICK) operates several of those night clubs and their earnings in three months will be interesting to watch. I am more hopeful tho, that I can pick up a good watch in the future without giving up both kidneys.

If you have enjoyed my article, please share and subscribe.

Enjoyed this newsletter, thank you!

Always a pleasure receiving your newsletters in my inbox